Cooperative Banks: The Financing Backbone of Grassroots India

When a small farmer in Maharashtra needs seeds before the monsoon, he rarely walks into a big private bank. Instead, he turns to his local cooperative bank, an institution woven into the fabric of rural India for over a century. Similarly, a vegetable vendor in Karnataka who wants to expand her stall finds her first credit lifeline at the cooperative counter, not a commercial branch.

In short, cooperative banks are not just financial institutions. They are community-owned, member-driven pillars that quietly finance the lives of millions at the grassroots, from farmers and artisans to small traders and daily wage earners.

What makes cooperative banks different?

Unlike commercial banks that chase shareholder profit, cooperative banks operate on the principle of mutual benefit. As a result, members act as both customers and owners. Moreover, decisions follow a democratic process, interest rates stay generally lower, and local needs always come first.

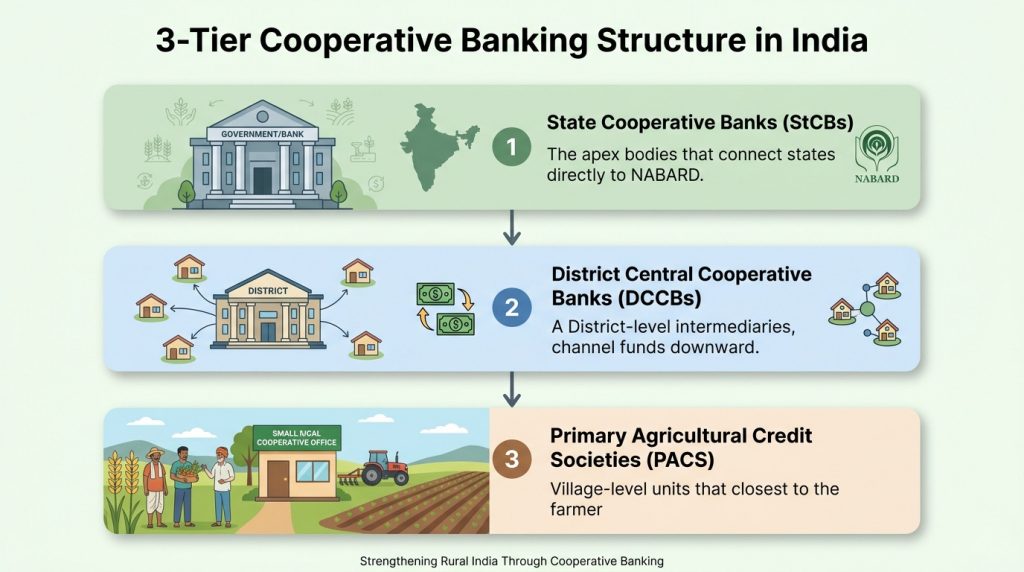

Furthermore, their structure operates across three clear levels:

- Primary Agricultural Credit Societies (PACS) — the village-level units, closest to the farmer

- District Central Cooperative Banks (DCCBs) — the district-level intermediaries that channel funds downward

- State Cooperative Banks (StCBs) — the apex bodies that connect states directly to NABARD

India hosts over 1,500 urban cooperative banks and nearly 96,000 PACS — together, they serve more than 290 million members across the country.

Why grassroot India still depends on them

Commercial banks have certainly expanded their reach. However, the last mile remains underserved. Consequently, cooperative banks step in to fill that gap with practical, community-rooted solutions:

- Simpler documentation that allows small farmers faster credit access

- Seasonal loans that align directly to crop cycles

- Local language support and long-standing personal relationships

- Lower interest rates under government-backed schemes like the Kisan Credit Card

Additionally, for Italy-based exporters who supply fresh produce to India, understanding cooperative bank financing matters greatly. Bulk buyers — importers, wholesale traders, and agri-cooperatives — often rely on cooperative credit lines to fund large seasonal purchases of imported fruits and vegetables. Therefore, knowing how these buyers access capital helps exporters plan supply cycles more effectively.

Cooperative banks vs commercial banks: a quick comparison

| Feature | Cooperative banks | Commercial banks |

|---|---|---|

| Ownership | Member-owned | Shareholder-owned |

| Focus | Rural, agri, small trade | Urban, corporate, retail |

| Interest rates | Generally lower | Market-linked |

| Documentation | Simpler, flexible | Stricter, formal |

| Reach | Deep rural penetration | Urban-centric |

Challenges they face today

Cooperative banks, however, carry real challenges. Governance gaps, rising NPAs, and slow technology adoption have weakened several institutions over time. In response, the RBI and NABARD have pushed through major reforms — notably bringing urban cooperative banks under direct RBI oversight since 2020.

Despite these challenges, their relevance holds firm. In fact, key government schemes like PM Kisan, PMFBY crop insurance, and e-NWR (electronic negotiable warehouse receipts) now increasingly flow through cooperative structures, reinforcing their central role.

The Italian connection: why this matters for agri-exporters

India’s appetite for premium imported produce — Italian tomatoes, specialty citrus, grapes, and processed vegetables, grows steadily each year. Furthermore, the buyers who power this demand often operate through cooperative or community-linked trade networks that cooperative bank credit actively supports.

Consequently, an Italian exporter who builds trade relationships with cooperative-bank-financed Indian importers gains access to more reliable, seasonal bulk orders. This proves especially true in Tier 2 and Tier 3 markets, where cooperative credit flows most freely and where demand for quality imported produce continues to rise.

Frequently asked questions

Q1. What is the role of cooperative banks in Indian agriculture?

Cooperative banks deliver affordable seasonal credit to farmers, helping them buy seeds, fertilizers, and equipment, especially in areas that commercial banks do not serve well.

Q2. Are cooperative banks safe to deposit money in India?

DICGC insures deposits up to ₹5 lakh. Additionally, the RBI now directly regulates urban cooperative banks, which significantly strengthens their safety standards.

Q3. How many cooperative banks are there in India?

India maintains over 1,500 urban cooperative banks and nearly 96,000 PACS, collectively serving hundreds of millions of members nationwide.

Q4. How do cooperative banks support rural traders and small businesses?

They offer working capital loans and trade credit with flexible documentation, making it easier for small vendors and rural entrepreneurs to access the financing they need.

Q5. Why should foreign exporters understand India’s cooperative banking system?

Many Indian importers and bulk agri-product buyers rely on cooperative bank credit. Understanding this helps exporters identify financially ready buyers in rural and semi-urban markets.

For more such insights on cooperative banks and rural finance in India, explore more articles on Cleuz and stay informed.