Understanding Cooperative Banking in India – Bankers to the Grassroots

Walk into a small village or a local market, and you’ll notice something interesting. Not everyone depends on big national banks. Instead, many people trust smaller, community-based banks that feel more personal and accessible.

These are Cooperative Banks, the real backbone of grassroots banking in India.

But what makes them so important? And why are they still relevant in a fast-moving digital world? Let’s break it down.

What are Cooperative Banks?

At the simplest level, cooperative banks are financial institutions owned and operated by their members. In other words, the customers are also the stakeholders.

Unlike traditional banks that focus mainly on profits, cooperative banks are built on community support and mutual benefit.

For example, a group of farmers, small business owners, or local residents come together to form a bank that serves their financial needs. As a result, the focus shifts from “profit first” to “people first.”

Why are they called “bankers to the grassroots”?

Because they reach where most banks don’t. Cooperative banks play a huge role in:

- Rural areas

- Small towns

- Local communities

While large banks may hesitate to lend to small borrowers, cooperative banks step in. They provide loans to farmers, small shop owners, and self-employed individuals who may not have strong financial records.

Therefore, they don’t just offer banking, they enable livelihoods.

Think about it this way:

If a farmer needs a small loan for seeds, a cooperative bank is often the first place they go.

Types of cooperative banks in India

To make things clearer, cooperative banks are broadly divided into two categories:

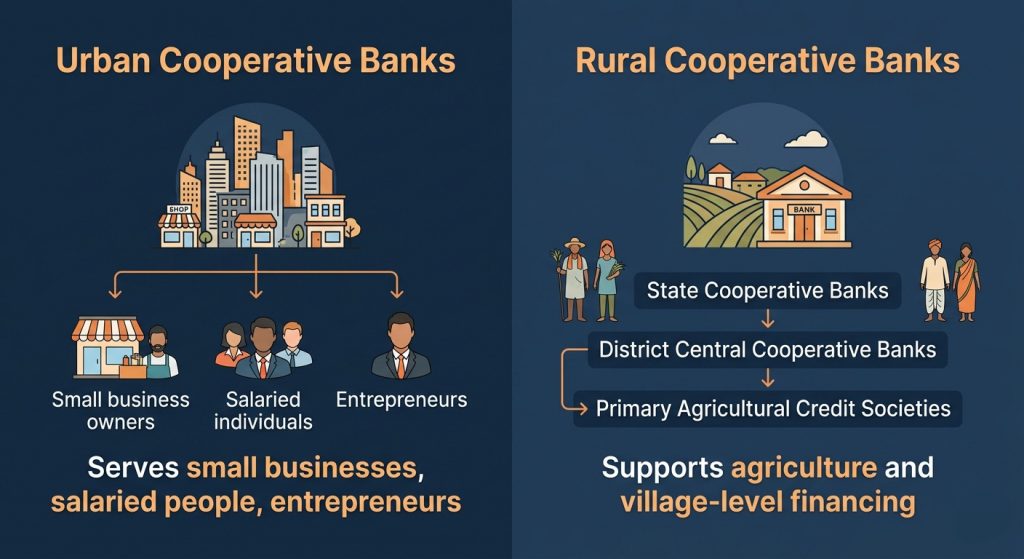

1. Urban Cooperative Banks (UCBs)

These operate in cities and towns. They mainly serve small businesses, salaried individuals, and entrepreneurs.

2. Rural Cooperative Banks

These focus on agriculture and village-level financing. They are further divided into:

- State Cooperative Banks

- District Central Cooperative Banks

- Primary Agricultural Credit Societies

Each level supports the next, creating a strong local financial network.

Why do people trust them?

Trust is everything in banking and cooperative banks build it differently. Firstly, they are locally managed. This means the people running the bank understand the community’s needs.

Secondly, they offer easier access to credit. Unlike large institutions, they don’t rely heavily on strict documentation.

Moreover, they promote financial inclusion. Many people who were previously outside the banking system get their first experience through cooperative banks. So, it’s not just about money, it’s about accessibility and familiarity.

The challenges they face

However, it’s not all smooth.

Cooperative banks often struggle with:

- Limited technology adoption

- Operational inefficiencies

- Regulatory challenges

Additionally, some banks face issues with transparency and management due to their local structure.

As the financial world becomes more digital, these challenges become even more noticeable.

The digital shift: A new opportunity

This is where things get interesting.

Today, technology is transforming how cooperative banks operate. Digital tools are helping them:

- Automate processes

- Improve customer experience

- Enable faster decision-making

For instance, modern digital solutions allow banks to generate reports instantly, track performance in real time, and manage operations more efficiently.

In fact, digital product labs are now building custom platforms and analytics tools that help cooperative banks function smarter and faster.

As a result, even small banks can now compete with larger institutions in terms of service and efficiency.

Why this matters today

India is still a country where a large population depends on local economies.

Therefore, strengthening cooperative banks means strengthening:

- Rural development

- Small businesses

- Financial inclusion

Moreover, when technology meets community-driven banking, the impact becomes even more powerful.

Imagine a farmer in a remote village accessing banking services through a mobile app powered by modern systems. That’s the future already taking shape.

Final thoughts

Cooperative banks may not always be in the spotlight, but their impact runs deep. They are not just financial institutions, they are enablers of growth at the grassroots level. So next time you think about banking in India, ask yourself: Is it just about big banks and digital apps… or also about the small institutions quietly supporting millions?

Because sometimes, the strongest systems are the ones built closest to the people. To stay updated on the latest in digital technology and practical insights, visit Cleuz Blog and explore more resources for forward-looking development.